An excellent real estate agent can help you learn the art of home buying, whether you want to buy a home by yourself or with a spouse or significant other.

- Get it in writing. If you don't have it in writing, prove that you own the property you want to borrow. No one will loan you more than you can afford.

- Find out what your mortgage amount is at the start of your loan. What loan amount is considered intermediate? If you borrow too much, it may not be a good idea to take out the loan.

- Talk to your lender about the current market conditions and what will happen over the next 30 years. Ask if the interest rate can be increased. Ask to be able to adjust the payments if the interest rate drops.

- Have your lender take into consideration your age, your projected career path, your income, your debts, and your lifestyle. If you can afford more, then, by all means, take out the loan. You will be able to pay off the loan and increase your home equity.

The best way to make sure that your life savings are safe is to make sure that your lender is a reputable company licensed and approved by the state. Ask a lot of questions and be very clear about what you are asking your lender to do. A trustful lender will take care of your loan.

I hope you found this article helpful? As you continue your quest for wealth and financial security, the investment strategies laid out in Think Like a Tycoon by Dr. W.G. Hill is the resource you should seriously consider.

Think Like A Tycoon by W.G. Hill

How to Make a Million in Three Years or Less

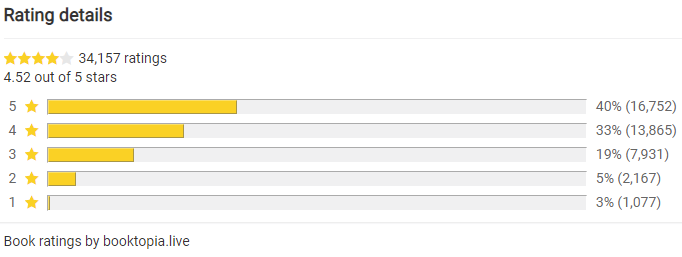

I am a real estate investor for 10 years now and personally involved in 40 real estate transactions. With that said, this is the book to read. Read this book if interested in real estate investing. Don't if you aren't.(Michael - Real Estate Investor)

…NOW is your golden opportunity to turn bargain property deals into 1 MILLION in just 3 years…

…using other people’s money and this property tycoon’s no-brainer strategy…

What you have to do to secure your future and avoid becoming another government statistic

It’s simple: Make your fortune from “distressed property”. And Dr. W.G. Hill can show you how.

For your convenience, we have added a link to Think Like A Tycoon on all the Amazon marketplaces, for the fastest delivery please choose your local marketplace. If "Currently unavailable" choose the marketplace nearest your location.

Note! Think Like a Tycoon is only available in English.

For your convenience, we have added a link to Think Like A Tycoon on all the Amazon marketplaces, for the fastest delivery please choose your local marketplace. If "Currently unavailable" choose the marketplace nearest your location.

Note! Think Like a Tycoon is only available in English.

America - Canada - Sweden - Germany - Italy - France - Spain - Poland - Netherland - Mexico - Brazil - India - Japan - Singapore - United Kingdom - Australia & UAE ships from the UK!) - Saudi Arabia - China -

Stay tuned for more free videos, articles, tools, and other valuable resources.

Please continue the conversation for this post on the

Think Like a Tycoon Forum - LinkedIn - Facebook

Stay tuned for more free videos, articles, tools, and other valuable resources.

Please continue the conversation for this post on the

Think Like a Tycoon Forum - LinkedIn - Facebook